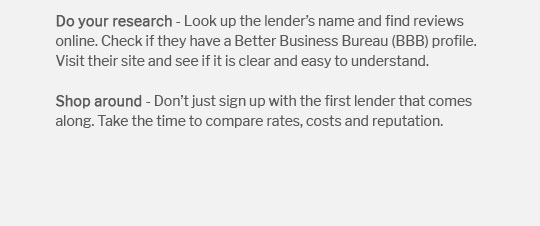

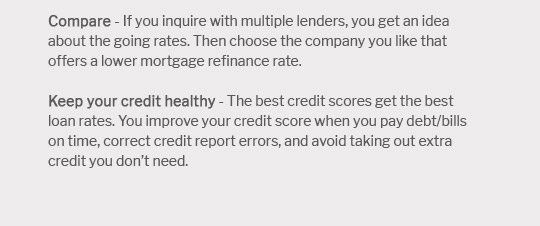

line of credit loan insights for taking control today

Market snapshot

We see lenders positioning flexible limits for on-demand cash flow. A line of credit loan lets you draw, repay, and redraw, paying interest only on what you use. It sounds easy, yet variable APR and fee schedules can nudge costs.

Where it fits

At 7 a.m., before a contractor arrived, we checked our available credit, drew for materials, and kept the project moving - action without selling assets.

- Compare a personal line of credit versus a business line of credit for tailored limits.

- Consider a HELOC when home equity lowers rates.

- Choose revolving credit with clear draw periods and repayment terms.

- Weigh secured vs unsecured access, collateral, and speed.

- LOC vs credit card: control larger purchases, often at lower rates.

Next step: review limits, rate caps, and covenants; act early if you'll need liquidity.